East Asia

Overview

East Asia is the historical heart of seaweed farming, where the practice began over 70 years ago, and it remains the world's leading seaweed-producing region today. China is the dominant force, accounting for approximately 90% of regional production and setting long-term trends across East Asia. South Korea is the second-largest producer and has steadily increased its output. In contrast, Japan, the birthplace of seaweed aquaculture, has seen a decline in production volumes over the past decade, primarily due to an aging farming population.

Seaweed production by country

Seaweed production: volume and value

Farmed species

The industry in East Asia is prominently dominated by three genera, each playing a critical role in the regional and global market:

Saccharina

(formerly known as Laminaria japonica)

Pyropia

(Nori)

Undaria

(Wakame)

The vast scale and biological diversity of farmed seaweed in East Asia are testaments to centuries of refinement in aquaculture techniques, driven by an unceasing cultural demand for this versatile and nutritious marine vegetable.

Production by species

Saccharina

Commonly referred to as 'kombu' in Japan, this brown algae is one of the most commercially significant seaweeds globally. Its cultivation is widespread, particularly in China and Korea, where it is used extensively. Saccharina is prized for its umami-rich flavour, making it an essential ingredient for dashi (soup stock), stews, and as a cooked vegetable. It is also a source of alginates and iodine.

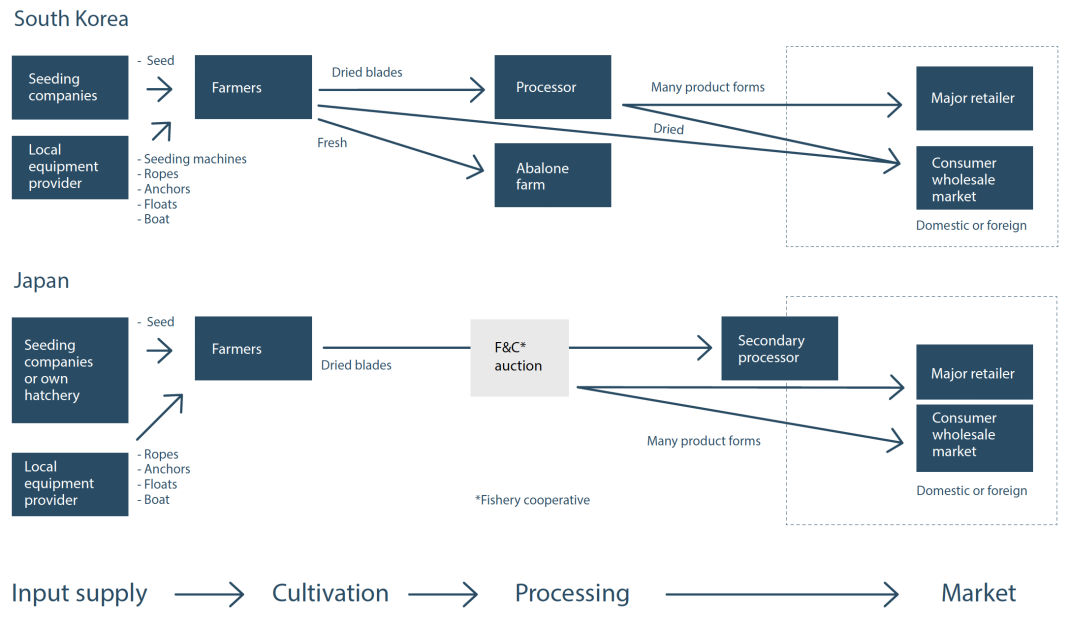

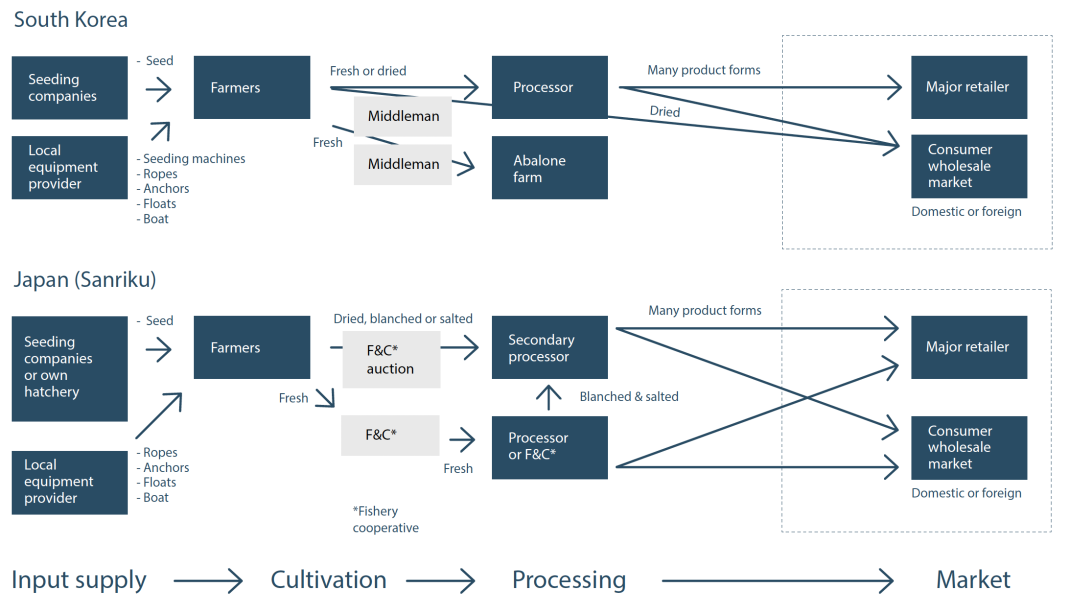

The high level supply chain overview for Saccharina

This supply chain illustration only applies to the two main uses for Saccharina today: human food and aquaculture feed. Alginate is mainly processed from wild harvested seaweed and therefore not included in this overview.

Input suppliers: farmers need equipment such as lines, ties, buoys and anchors, as well as seed material from dedicated seed companies or their own hatcheries. Equipment is easily available through local shops, which

provide all materials required to build the cultivation system.

Farmers: either companies or family farmers. Learn more about the farmers and the cultivation process in our farm insights chapter. In Japan and South Korea most Saccharina farming is done by family farmers.

In Japan being part of a fishery cooperative is mandatory and all product sales go through the auctions organised by the cooperative.

In South Korea roughly 70% of the Saccharina is sold directly to neighbouring abalone farms as fresh feed. The rest is sold to processors that turn the seaweed into a variety of product forms for human consumption through

retail stores and consumer wholesale markets.

In Japan, retailers and consumer wholesalers participate in the auctions of the fishery cooperatives to secure their supply of Saccharina products, which are then sold on to restaurants, or directly to consumers for consumption at home.

Explore the way Saccharina is farmed step-by-step here

Pyropia

This is arguably the most famous and recognizable seaweed internationally, instantly associated with the iconic wrap for sushi and onigiri (rice balls). Known as 'nori' in Japan and 'gim' in Korea, Pyropia species are fast-growing red algae cultivated on nets suspended in the water. The dried, pressed sheets are a staple food, valued for their crisp texture, dark green colour, and delicate, slightly sweet flavour.

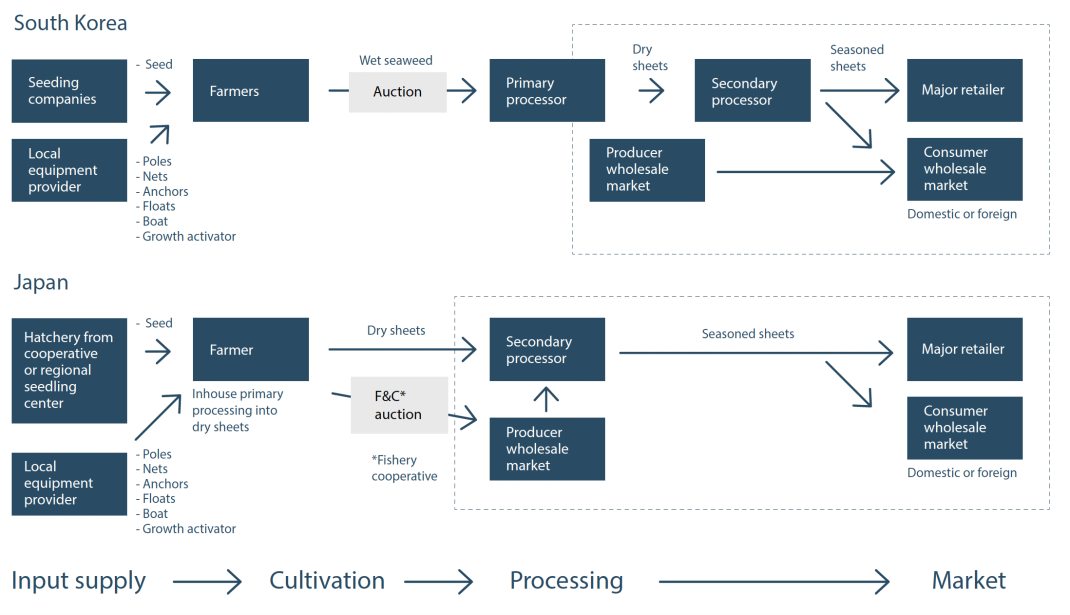

The high-level supply chain overview for Pyropia

Input suppliers: farmers need equipment such as lines, ties, buoys and anchors, as well as seed material from dedicated hatcheries. Equipment is easily available through local shops, which provide all materials required to build the cultivation system.

Farmers: either companies or family farmers. Learn more about the farmers and the cultivation process in our farm insights chapter. In Japan and China, the primary processing is usually carried out by farmers or farming companies themselves with an automatic machine for dry nori sheet production.

Fisheries cooperatives: in South Korea all Pyropia farmers sell the freshly harvested seaweed straight from the harvesting vessel through the auctions that take place every morning during harvest season at the farmers’ cooperative port. In Japan, these sheets are sold through open tenders at the fishery cooperative’s auction and sent to department stores, restaurants and supermarkets.

Processors turn Pyropia into dry sheets, seasoned sheets or other types of snack products and sell packaged Pyropia products to wholesale markets and retail stores that sell them onwards to restaurants or directly to consumers for consumption at home.

Explore the way Pyropia is farmed step-by-step here

Undaria

Known as 'wakame,' this highly popular brown seaweed is a ubiquitous ingredient in various East Asian cuisines, most famously in miso soup and salads. Undaria is known for its subtly sweet flavour and distinctive, slippery texture. Its high nutritional profile, particularly its content of vitamins, minerals, and the pigment fucoxanthin, contributes to its perceived health benefits and widespread consumption across the region.

The high-level supply chain overview for Undaria

This supply chain illustration only applies to the two main uses for Undaria today: human food and animal feed.

Input suppliers: farmers need equipment such as lines, ties, buoys and anchors, as well as seed material from dedicated seed companies or their own hatcheries. Equipment is easily available through local shops, which provide all materials required to build the cultivation system.

Farmers: in South Korea, farmers typically belong to a “Fishing Village Contract” and have private farms. However, these types of farms, especially in the southern province of Jeonnam, can be large scale with several employees. In Japan, all farmers are cooperative members, while everyone has their own unit they are working on. Almost all farmers run small operations in a family-based household industry. Learn more about the farmer and the cultivation process in our farm insights chapter.

In South Korea, roughly 60% of the farmed Undaria is directly sold to neighbouring abalone farms as fresh feed. The rest is sold to processors. For the domestic market, processing factories for drying, salt preservation are the main buyers. Processed Undaria is sold in a variety of product forms for human consumption, through retail stores and consumer wholesale markets.

In Japan’s Sanriku region, all blanched, salted, dehydrated and dried Undaria products are sold through auction by JF Zengyoren (National Federation of Fisheries Co-operative Associations) where retailers and consumer wholesalers participate and distribute it on to restaurants, or directly to consumers for consumption at home.

Explore the way Undaria is farmed step-by-step here

China

Overview

China’s seaweed production has seen significant expansion over the past decade. This growth in volume was accompanied by a similarly strong upward trend in production value. While the industry's total worth reached its highest point recently, a slight dip in the most recent year, despite continued volume increases, suggests a mature, high-output market undergoing changes in pricing and overall dynamics.

Saccharina (Kelp): This species dominates the sector, reaching an impressive 12 million tonnes in 2023. Its production reflects consistent growth, solidifying its strategic role in both the food supply chain and the supply of phycocolloids (alginates). However, this growth trajectory is increasingly exposed to environmental pressures, highlighted by episodic losses.

Gracilaria: Unlike the other major species, Gracilaria production shows stagnation. Its growth is hindered by increasingly tightening coastal regulations, which restrict the permissible area and methods for its cultivation.

Undaria (Wakame): Production of Undaria has climbed to approximately 2 million tonnes. This expansion is primarily driven by rising domestic demand for this high-value food species, indicating a growing consumer preference for premium seaweed products.

Pyropia (Nori/Laver): Pyropia production remains stable at around 2 million tonnes. Further significant expansion for this species is severely constrained by spatial limitations, as suitable coastal areas are finite, and by strict regulatory restrictions that limit the establishment of new farming zones.

Explore the way Saccharina, Gracilaria, Undaria, and Pyropia are farmed in China step-by-step

Future production outlook

China’s seaweed industry continues to show strong growth potential, underpinned by robust and increasing domestic demand, particularly for premium species like Saccharina and Undaria that supply critical food and phycocolloid value chains. However, this expansion is increasingly constrained by strict coastal regulations, climate-driven disturbances, and intense spatial competition with other marine industries. Significant environmental risks, exemplified by red-tide losses exceeding 30 million USD, further threaten production stability.

Long-term resilience and value creation will depend on:

Implementing integrated marine spatial planning to resolve conflicts

Advancing technological innovation for climate resilience & efficiency

Fostering greater coordination between aquaculture, environment & other marine sectors

By advancing these priorities, China can navigate its complex coastal pressures to secure the continued growth, modernisation, and environmental sustainability of its world-leading seaweed sector.

South Korea

Overview

A lot of investment has gone into the Korean supply chain, not least driven by a strong national preference for seaweed cultivation (more as a matter of food security/ food sovereignty compared to climate or health benefits). Strong local government public support that includes financial and preferential tax and zoning components that dovetails with regional and national government support.

In South Korea, only fishermen who hold aquaculture licenses are allowed to grow seaweed and it is controlled by the local government. Compared to Japan though, companies were allowed to operate, resulting in an increasingly industrialised and segmented industry which specialised areas such as production, processing, distribution and export.

As a result, South Korea's seaweed industry has shown substantial growth in production over the last decade. Output climbed consistently for several years, reaching a peak recently before experiencing a slight dip. Despite the variability in financial returns, the industry maintains a high level of output and remains economically significant.

Unique to South Korea are the species specific hatcheries that provide high quality seed for the main species (Pyropia, Undaria and Saccharina), where now 95% of seed comes from private hatcheries. Since the 2000s, South Korea has seen an annual increase in the production of Undaria and Saccharina seaweed, a trend largely fuelled by the consistent demand for abalone feed.

Saccharina (Kelp): Is the largest farmed seaweed category in South Korea, reaching about 596,000 tonnes in 2023. Around 65% of this production is used as abalone feed, reflecting its central role in the aquaculture feed industry.

Pyropia (Nori): Pyropia production totaled approximately 533,000 tonnes in 2023. Nearly all output is directed toward human consumption, mainly exported as dried sheets, and demand for this species continues to rise.

Undaria (Wakame): Undaria production reached about 567,000 tonnes in 2023. It remains valued for direct human consumption in salads, soups, and side dishes across East Asia, but around 60% of production is also used for abalone feed.

Explore the way Saccharina, Undaria, and Pyropia are farmed in South Korea step-by-step

Other species production

In addition to the main species, South Korean farmers also cultivate:

- Sargassum fusiforme (human consumption)

- Costaria costata (abalone feed and marine restoration)

- Codium

- Eisenia

- Gracilaria

Multi-species farming is common in southern regions such as Wando and Jindo, particularly among brown seaweed producers. This strategy responds directly to the abalone industry’s need for a year-round supply of fresh feed:

- Saccharina: December to August

- Undaria: November to April

Species such as Costaria costata are being developed to bridge the critical September–October feed gap, when kelp availability is lowest.

Future production outlook

South Korea’s seaweed industry is a mature, technologically advanced sector characterized by a dual structure: high-value Pyropia (nori) production for direct human consumption and Saccharina (kelp) cultivation integrated with abalone aquaculture. However, growth is constrained by severe nearshore space saturation, a government freeze on new concessions, and chronic labor shortages. In response, the industry has strategically pivoted from pursuing volume to prioritizing quality and yield stability, with offshore expansion emerging as the only viable long-term pathway for growth.

Long-term resilience and controlled expansion will depend on:

Accelerating the development and adoption of offshore cultivation systems

Advancing genetic innovation for climate resilience and extended harvest seasons

Modernising practices to improve labour efficiency and attract new workforce

By advancing these priorities, South Korea can leverage its advanced breeding programs—including 15 government-certified varieties—and technological expertise to overcome spatial and labor constraints, securing the future of its high-value seaweed sector and its critical link to the abalone industry.

Japan

Overview

Over the past decade, Japan's seaweed industry has experienced a significant transformation. Although the quantity of seaweed harvested has steadily declined, this contraction has coincided with substantial growth in the overall worth of the industry. This trend suggests a strategic pivot toward premium offerings, where increasing prices and a shift in the types of products sold are fueling a major rise in the sector's economic value, even as the production base shrinks.

Japanese Saccharina is a premium specialty seaweed rather than a bulk commodity. Its production has declined steeply over time, falling from 230,000 tonnes in 1992 to roughly 26,000 tonnes in 2023, a trend intensified by ageing farmers and limited succession in key producing regions.

Undaria is traded exclusively through fishery cooperative auctions that define Japan’s official market assessments. Domestic output has decreased to around 50,000 tonnes in 2023, with roughly 80% of national demand now supplied through imports, primarily from China and South Korea.

Pyropia sector is highly structured, with all production marketed through fishery cooperatives. Output has declined from a 480,000-tonne peak to about 201,000 tonnes in 2023, and future production is limited by labour shortages tied to an ageing workforce and low automation.

Future production outlook

Japan’s seaweed industry operates a premium, processing-focused model centred on high-value species like Pyropia (nori) and Undaria (wakame). However, the sector faces mounting structural constraints, with production of these and other key species like Saccharina (kombu) in sustained decline due to an aging workforce, chronic labour shortages, and an increasing reliance on imports. Although the industry has successfully raised total value through processed and premium products, its long-term sustainability requires fundamental modernisation to maintain a viable, though likely smaller, high-value domestic sector.

Long-term resilience and continuity will depend on:

Accelerating the automation of cultivation and processing to offset labour shortages

Diversifying and deepening the portfolio of premium, value-added products

Implementing strategies to attract and secure a skilled workforce

By advancing these priorities, Japan can leverage its advanced technology and strong market to navigate its demographic challenges and preserve a resilient, high-value seaweed industry for the future.