South East Asia

Overview

Southeast Asia’s seaweed sector is a high-volume regional powerhouse dominated by Indonesia, the world’s leading eucheumatoid producer. The Philippines remains a major contributor but with highly variable annual output, while Malaysia operates at a smaller scale yet shows capacity for sharp rebounds in production. Across all three countries, the industry is narrowly based on eucheumatoids and increasingly Gracilaria production, underscoring Southeast Asia’s central role in the hydrocolloids supply chains.

Seaweed production by country

Seaweed production: volume and value

Farmed species

Southeast Asia’s seaweed industry is biologically dominated by eucheumatoid species

Eucheumatoids

(Kappaphycus and Eucheuma)

Gracilaria

Production by species

Eucheumatoids

Eucheumatoids form the backbone of tropical seaweed farming, producing about 10.2 million tonnes in 2023. Their main commercial value lies in carrageenan extraction for food, pharmaceutical, cosmetic, and nutraceutical uses. A small share, mainly Eucheuma denticulatum, is eaten fresh. Notably, 70–92% of the nutrient-rich biomass remaining after extraction is discarded, representing substantial lost value.

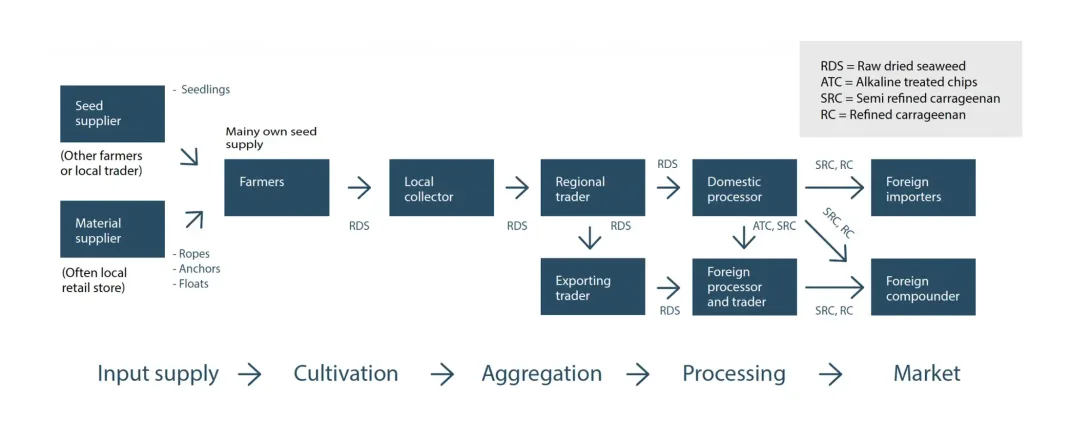

The high level supply chain overview for Eucheumatoids

Eucheumatoids are often farmed in quite remote areas across the coral triangle region. Only the close-knit network of all value chain actors makes this possible.

Input suppliers: Farmers need equipment such as lines, ties, buoys and anchors, as well as seedlings. Equipment is easily available through local shops which provide all materials required to build the production system.

Farmers: These are almost exclusively smallholders from coastal communities who farm seaweed either full-time or part-time to provide a livelihood. Learn more about the farming process in our farmer insights chapter.

Collectors and local traders: Well connected local actors who will buy the seaweed from the farmers and aggregate volumes to further trade. Prerequisites include a vehicle for transport of the seaweed and a warehouse. Some handle only small volumes and are seaweed farmers themselves, others are fully dedicated to the trade activity and have several employees. Activities of local collectors include buying semi-dried seaweed, bringing it to a warehouse, cleaning, sorting, sun drying to reduce the moisture content to a percentage that meets the requirements of the exporters and processors, packaging and transportation to a regional trader.

Regional traders: Often located in the major port cities, they can be independent or work for a processor or exporter. They often dry the seaweed again, clean again, store the seaweed in the warehouse and transport raw dried seaweed to an Indonesian domestic processor or to an exporter in compressed bales of roughly 100 kg.

Exporting traders: These traders primarily supply dry seaweed to foreign markets and a smaller amount to domestic processors. They often pay local traders in cash, pre-payments and working capital.

Processors: Today almost all processors of Eucheumatoids produce carrageenan (semi-refined and refined carrageenan in different types of grading). For all products the seaweed is washed to remove sand, salts and other foreign matter before several processing steps are applied.

Compounder & Ingredient manufacturers: Will buy the refined or semi-refined carrageenan from processors as an input ingredient for blends which are dedicated to the production of specific products across the food, nutraceutical, pharmaceutical and cosmetic industries.

Disclaimer: National- and regional-level differences do exist and the individual networks impact the production.

Explore the way Eucheumatoids are farmed step-by-step here

Gracilaria

Gracilaria is the second major farmed seaweed in East Asia, though produced at much lower volumes than Eucheumatoids, yielding just over 2 million tonnes in 2023. Its primary commercial value lies in agar extraction for food, pharmaceutical, and biotechnology uses. A small portion is consumed fresh. Notably, limited pond capacity constrains production, highlighting strong potential for expansion through sea-based farming.

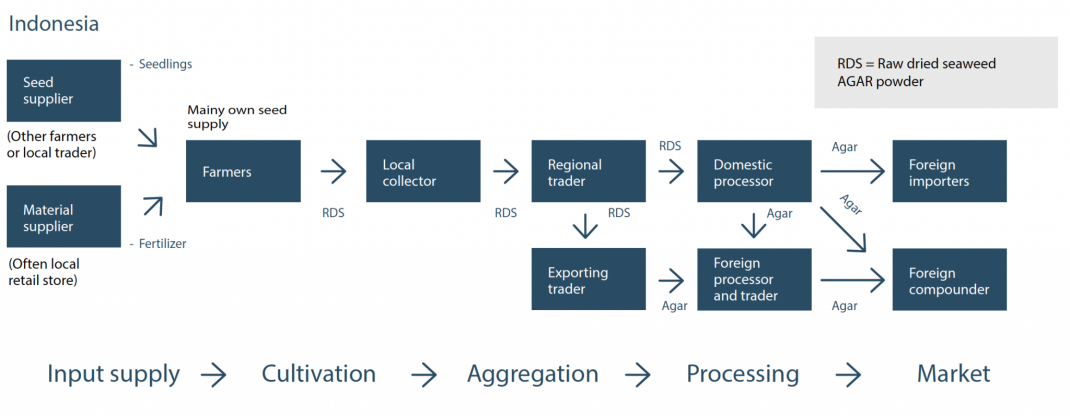

The high-level supply chain overview for Gracilaria in Indonesia

Input suppliers: pond-based Indonesian Gracilaria farmers typically don’t have many material needs. They get the seedlings from their own harvest or other farmers or the local collectors. Once in a while they might purchase fertiliser from a local agri-inputs trader.

Farmers: these are almost exclusively smallholders from coastal communities who farm seaweed either full-time or part-time to earn a living. Learn more about the farming process in our farm insights chapter.

Local collectors: well connected local actors who will buy the seaweed from the farmers and aggregate volumes to further trade. The prerequisites are a vehicle for the transport of the seaweed and a warehouse. Some handle only small volumes and are seaweed farmers themselves, others are fully dedicated to the trade activity and have several employees. Activities of local collectors include buying semi-dried seaweed, bringing it to a warehouse, cleaning, sorting, sun drying to bring the moisture content to a percentage that meets the requirements of the exporters and processors, packaging and transportation to a regional trader.

Regional traders: often located in the major port cities, they can be independent or work for a processor or exporter. They often dry the seaweed again (re-drying), remove impurities, pack it manually, store it in the warehouse and transport raw dried seaweed to Indonesian domestic processors or to the exporters.

Exporters: the exporters primarily supply dry seaweed in compressed 50 kg bales to foreign markets and a smaller amount to domestic processors. They often pay local collectors and regional traders in cash (bank transfer), and provide down payments and working capital to local collectors and regional traders.

In 2021 almost 50% of all Gracilaria produced in Indonesia (37.000 tonnes dry weight, equivalent to 353.000 tonnes wet weight) was exported according to official statistics. China is by far the main importer of dried seaweed from Indonesia.

Processors: almost all processors of Gracilaria currently produce agar. For this process seaweed is washed to remove sand, salts and other foreign matter before several processing steps are applied for extracting the agar. In 2021 a little over 50% was processed domestically in Indonesia (47.200 tonnes dry weight, equivalent to 600.000 tonnes wet weight) according to the Indonesian Seaweed Industry Association. China is by far the main importer of dry seaweed from Indonesia.

Explore the way Gracilaria is farmed step-by-step here

Indonesia

Overview

Indonesia’s seaweed sector remains one of the world’s largest but is marked by pronounced volatility, with production rising from around 1.2 million tonnes in 2014 to nearly 1.9 million tonnes in 2022 before contracting sharply in 2023. Official figures citing as much as 7 million tonnes in 2021 contrast with industry estimates of 1.3–1.5 million tonnes, underscoring persistent data discrepancies alongside a recent downturn reflected in market value falling from USD 365.7 million in 2022 to USD 126.3 million in 2023.

Eucheumatoids are a high-volume commercial crop rather than a niche species. Their production climbed rapidly to a 10-million-tonne peak around 2018 before contracting to about 8 million tonnes in 2023, a trend shaped by uneven regional performance and persistent seed and disease challenges.

Gracilaria is a rapidly expanding farmed seaweed rather than a minor crop. Its production has risen from modest levels in the 2000s to around 1–2 million tonnes in 2023, a trend supported by strong demand and large unrealised potential for expansion through sea-based cultivation.

Overall, Indonesia’s species-level trends reflect sustained high-volume cultivation centred overwhelmingly on eucheumatoid farming.

Future production outlook

Indonesia remains the world's largest producer of Eucheumatoid seaweed, yet its growth is increasingly constrained by systemic pressures. Climate shocks, persistent disease, declining seed quality, and fragmented, low-value supply chains threaten productivity in traditional growing regions. While expansion continues in newer areas, it does so amid volatility. Government plans for seaweed industrialization zones and the potential of Gracilaria cultivation offer pathways for modernization, though the latter is pushing development toward more complex sea-based systems.

Long-term resilience and value creation will depend on:

Implementing marine spatial planning & climate-resilient farming methods

Developing disease-resistant, high-yield seedstock through genetic improvement

Expanding local processing capacity in industrialisation zones to capture more value

By advancing these priorities, Indonesia can transition its massive production base from a vulnerable, commodity-focused model into a more technologically advanced, diversified, and resilient industry capable of securing greater value and stability for its coastal communities.

The Philippines

Overview

The Philippines’ seaweed industry exhibits considerable fluctuation, with production peaking in 2011 and rising again by 2018 before declining and partially recovering through 2023. Industry estimates are often far lower than official statistics, underscoring uncertainty in output levels. Market value mirrored these shifts, rising, dropping sharply, and later recovering, leaving the sector defined by high volumes but persistent instability.

The Philippines’ seaweed sector is overwhelmingly dominated by Kappaphycus alvarezii and Eucheuma spp., which account for virtually all farmed output. Production has remained consistently high, while Gracilaria contributes only marginal volumes. Overall, the country’s species profile reflects a heavily concentrated industry in which eucheumatoid cultivation underpins national supply and defines the structure of the farmed seaweed sector.

Future production outlook

The Philippines, the historic pioneer of commercial Eucheumatoid seaweed farming, possesses a deep-rooted foundation for production. However, near-term growth is severely constrained by compounding environmental and socio-political vulnerabilities. The northeastern production zones face severe seasonal limitations due to frequent typhoons, while the primary southern producing regions of Zamboanga and Tawi-Tawi are hindered by chronic political and social unrest, which stifles the investment and stability needed for expansion.

Long-term resilience and the revitalisation of growth will depend on:

Developing climate-resilient farming methods for typhoon-prone areas

Fostering stability & security to enable investment in core production zones

Diversifying products and improving supply chain value retention

By addressing these priorities, the Philippines can leverage its extensive experience to overcome systemic barriers and reclaim a trajectory of sustainable growth in its foundational seaweed sector.

Malaysia

Overview

Malaysia’s seaweed sector shows a substantial production base, with official data beginning near 270,000 tonnes before several years of contraction. Industry estimates as low as 30,000 tonnes in 2021 contrast sharply with the official 178,900-tonne figure. Recent output surpassing 300,000 tonnes and a fivefold value increase since 2018 indicate strong recovery despite persistent data discrepancies.

Malaysia’s farmed seaweed sector is overwhelmingly dominated by eucheumatoids, especially Kappaphycus alvarezii, which consistently drives national production. Output has remained largely high and stable, while minor groups such as Eucheuma espinosa and other seaweeds contribute only marginal volumes. This species composition reflects a highly concentrated industry shaped by reliance on a single commercially valuable eucheumatoid crop.

Future production outlook

Malaysia’s seaweed industry has significant expansion potential, bolstered by government initiatives aimed at scaling Eucheumatoid farming and enhancing export-oriented production. However, long-term growth and stability are hindered by deep structural weaknesses. The sector depends heavily on a legally insecure, non-citizen workforce, creating operational and social vulnerabilities. This foundational instability, combined with recurrent poor seed quality, climate-related production risks, and fragmented, low-value supply chains, severely limits productivity and commercial resilience.

Long-term sustainability and higher-value growth will depend on:

Formalising and stabilising the labour force through improved policies & training

Investing in domestic, high-quality seedstock and climate-resilient farming methods

Developing integrated local processing for value-added products & stronger market linkages

By addressing these priorities, Malaysia can transform its seaweed sector from a vulnerable, commodity-focused activity into a more secure, productive, and sustainable pillar of its coastal blue economy.